This week’s video transcript summary is here. You can click on any bulleted section to see the actual transcript. Thanks to Granola for its software.

Note: This Week’s Video is completely AI Generated. Andrew is away, so I created a fake (a deep fake). It’s pretty bad

Editorial

Last month I wrote about Human Agentcy. The spelling mattered. I was trying to describe something more specific than “agents” and less passive than “automation.” Agentcy is human agency extended through software that can act.

The point was not that AI replaces human agency. It was almost the opposite.

Extension, not replacement. Delegation, not autonomy.

That now feels like the center of this week.

The first phase of generative AI was about tools. A chatbot could write, summarize, code, search, explain, or draw. The second phase is about agents. Agents do not just answer. They enter workflows, use tools, make calls, run loops, invoke other agents, and return later with results. They turn software from something we operate into something that operates on our behalf.

That sounds like the human role should get smaller. I think it gets bigger.

The skill requirement goes up, not down.

Google’s Sundar Pichai made the interface change explicit. The old internet was built around browsers, search boxes, tabs, forms, and pages. The agentic internet is built around delegation. Instead of visiting a website, finding the right page, filling out 18 fields, uploading a document, and checking back later, an agent does the chore.

The line that stuck out was:

“Once you get the taste of the superpower that comes with agents... you realize they aren’t just tools, they are agency.”

That is the right word. Agency. But it is not agency floating in the air. It has to be designed, constrained, audited, and improved. If an agent renews your license, patches your code, routes your customer issue, or launches a database, the important question is not whether the agent can do the task once. The important question is whether the environment around it makes the action reliable.

Databricks CEO Ali Ghodsi gave a second proof point. According to the clip circulating this week, more than 81% of new Databricks databases are now being created by autonomous agents rather than humans. That is not a forecast. It is an operating fact inside a major enterprise data platform.

His line was even sharper:

“Writing software is ten times faster now... your margin is my opportunity.”

That is the old software industry hearing the new one knock on the door.

If software can be created ten times faster, barriers to entry fall. If agents are the primary users of a platform, product design changes. If workflows can be assembled and reassembled by small teams, coordination becomes the bottleneck. The advantage moves away from simply owning a large application and toward owning the loop, the data, the judgment, and the operating system around the agent.

That is why Dan Farrelly’s “Agent Loop Architecture” is more important than it may first appear. It is not merely a developer note about infrastructure. It is a map of the new work.

Farrelly says the agent stack has three layers: loop, skill, orchestrator. A loop is a repeated timed job, plus a decision-maker. A ‘skill’ is a durable workflow. The orchestrator is the engine that checkpoints steps, retries failures, stores run history, enforces concurrency, and lets new functions deploy without breaking work already in flight.

His cleanest summary is this:

“The loop is plumbing. The asset is the skill it calls.”

And the operational requirement is just as plain:

“These things have to survive a restart.”

This all sounds technical, but it is a job definition. A new job. This isn’t an engineer coding. This is a human designing workflows carried out by human designed agents. If you can walk in to any company and learn, and then automate, its workflows, you have the skills for the new job. It involves learning, listening, designing, articulating and delivering actual outcomes. And things are moving so fast, you will redo the whole thing in six months tops.

In the old software world, skill meant knowing the app, the workflow, the data, and the business rule. In the agent world, skill means knowing what should be delegated, designing the loop, choosing the right model and tool mix, setting constraints, auditing traces, catching errors, and improving the skill library over time.

The valuable worker is no longer the software engineer, or the operator of software. It has transformed into the designer and governor of agent environments.

That creates new jobs, or at least new definitions of existing jobs. Agent operator. Loop designer. Skill builder. Agent ops. Eval designer. Context architect. Model router. Human governor. These sound like awkward titles today because we are at the beginning of the transition. So did “social media manager” once. So did “cloud architect.” So did “data engineer.”

The deeper point is that the best human work lives outside of the code base and lives in strategy and execution. The person who once completed a workflow now designs the loop that completes it. The person who once checked a report now defines the evaluation that tells whether the report is good. The person who once remembered how the company works now encodes that memory into a reusable skill that survives a model swap, a process restart, or a change in vendor.

Satya Nadella’s phrase for this is “token capital.” The phrase is useful because it points to a new form of institutional wealth. A company has human capital, the knowledge and judgment accumulated by people. It also now has token capital, the workflows, traces, prompts, evals, skills, permissions, and agent loops that capture how work gets done.

The moat is not the model. Models will change. Prices will change. Capabilities will change. The moat is the learning, and permanent updating system, around the model.

Anthropic, Databricks, Z.ai, Google, Mutiny, and the open-source model companies all belong in the conversation. They are not separate AI stories. They are pieces of the same migration.

Anthropic is trying to control the safety and use boundary around frontier models. Z.ai is pushing long-horizon open models into coding-agent territory. Google is turning agents into an interface layer. Databricks is seeing agents become real users. Mutiny is refounding a SaaS company around an agent rather than a UI. Farrelly is describing the orchestration layer required to make all of this production-grade.

The question underneath all of it is simple:

Who owns the overview, and the loop?

Does the model company own it? Does the cloud own it? Does the app own it? Does the enterprise own it? Does the individual own it?

That question may matter more than who has the best chatbot this month. And the answer is - one or more humans own it. With new job titles.

There is another human lesson here. Ihtesham Ali’s post about Sam Altman’s Stanford remarks captured an uncomfortable point. Altman said the experts who were most certain scaling would not work were often the ones most unable to update when the data changed. The problem was not intelligence. It was identity.

The line I would keep is:

“The moment a belief becomes who you are, it stops being something you can update.”

That applies directly to the agent era.

If your identity is “I am the person who does this task,” an agent feels like a threat. If your identity is “I am the person who knows how this outcome should be achieved,” an agent becomes leverage. If your identity is tied to the current workflow, you defend the workflow. If your identity is tied to judgment, you redesign it.

That is why the new skill is not just using AI. It is staying updateable, or being open to continuous learning.

The AI era will make low-skill use easier. Anyone will be able to ask for a summary, a spreadsheet, a landing page, or a piece of code. That is real. But high-skill use will become more valuable, not less. Someone has to know whether the summary is faithful, whether the spreadsheet matters, whether the landing page sells, whether the code is safe, whether the loop should run, whether the permission should be granted, and whether the system is improving or merely doing more things faster.

This is where Paul Graham’s essay this week aligns with the agent discussion. Graham says startup wealth can be earned when founders make something users like enough to tell their friends about it. He ends with the claim that for startups, “the key is not exploitation but empathy.” Knowing what is wanted, and needed.

That remains true in an agent world. The best loops will not be the ones that simply replace human action. They will be the ones built by people who understand what other people need, where judgment belongs, where automation helps, and where it must stop.

Human agency does not disappear when agents arrive. It becomes more architectural.

The job is no longer just to use software. The job is to define what software should be allowed to do. And then to build the loop that lets it do it well.

Your job title is a liability. Your skills are growing. Redefining yourself is the most important small change you can do.

Contents

Editorial

Essays

How to Earn a Billion Dollars - Paul Graham

Technology and Social Change - Paul Krugman

How should we tax internet countries? - Madison Karas

Yes, let’s abolish federal governments - Elle Griffin

Notes on Egypt - Nick Corvino

A review of Neil Postman’s Amusing Ourselves to Death - Danny Crichton

With the World Cup looming, there’s still no clear replacement for sports Twitter - Andrew Webster

Like All Good Things, Sports Are Owned by the Rich Now - Freddie deBoer

AI

How to help knowledge workers who lose their jobs to AI - Casey Newton

The Taxman Is Coming for A.I. - Peter Coy

Frictionful Intelligence - Moses Sternstein

Google CEO Sundar Pichai says agents are becoming the new entry point to the internet - Henrikh / Sundar Pichai

Welcome to the AGI era of AI governance - Nathan Lambert

Anthropic’s Safety Superpower - Ben Thompson

Can open-source beat OpenAI? - Kinling Lo

The Geometry of Denial - Mark Daley

ChatGPT’s market share slips below 50% for first time - Ivan Mehta

Exclusive: OpenAI Losses Increased Nearly 8X in 2025, With Spending Hitting $34 Billion - Ed Zitron

Why is Meta destroying its engineering organization? - Gergely Orosz

Venture

Encyclopedia Galactica - Dan Gray

Taking Stock of the Seed Stage - Nnamdi Iregbulem

New Media, One Year In - Erik Torenberg

#349: The Rise of GP-Led Secondaries - Doug Dyer

SpaceX IPO: The Investor Who Never Sold a Share - Molly O’Shea with Justin Fishner-Wolfson

SpaceX passes Amazon as valuation balloons to $2.7T - Sean O’Kane

Booking.com of robotaxi - Jan-Erik Asplund

Databricks Widens the Lead on the Yellow Brick Token Path - Tom Tunguz

The Founder Who Lit $10M On Fire, With Mutiny’s Jaleh Rezaei - Alex Konrad with Jaleh Rezaei

Regulation

The White House’s shambolic AI policy - Gary Marcus

Europe reacts to Anthropic halting access to top AI models - Nathan Rennolds

Starmer to announce ‘Australia plus’ ban on social media for under-16s - Jessica Elgot, Dan Milmo and Aisha Down

Further CMA action to secure a fairer deal for businesses and improve Google search services in UK - Competition and Markets Authority

Apple announces major App Store changes for Brazil, including alternative app marketplaces - Marcus Mendes

Infrastructure

Data center opponents have blocked or delayed projects worth nearly $130 billion in 2026, study finds - Allan Smith

The US Government Is Letting a Key Data Center Regulation Expire - Vittoria Elliott and Molly Taft

Public and Private Medical Community Targeted by China-Nexus Threat Actor Pursuing Artificial Intelligence, Cyber, Medical, and National Defense Research - Patrick Whitsell and John McGuiness

How software development’s speed obsession enabled TeamPCP’s chaos crusade - Matt Kapko

SpaceX alum nabs $22M to turn rocket engines into geothermal power plants - Tim De Chant

Converting Coal Plants to Natural Gas - Brian Potter

How to fix transit construction in America - Matthew Yglesias, Will Poff-Webster and Arnab Datta

Chile turned to China for an undersea cable. The U.S. said no - Juan Ortiz-Freuler

Can America Build Nuclear Again? Part 2 - Roger Pielke Jr.

Can America Build Nuclear Again? Part 3 - Roger Pielke Jr.

Interview of the Week

The Trouble with Trillionaires - Andrew Keen with Mordecai Kurz

Startup of the Week

Post of the Week

Essays

How to Earn a Billion Dollars

Paul Graham | PaulGraham.com | June 2026

Paul Graham’s Oxford Union talk argues that it is possible to earn a billion dollars through a startup without cheating or exploitation. He says the mechanism is exponential growth: a founder’s ownership becomes extremely valuable when a company grows quickly for long enough in a large market. He illustrates the math with a startup growing 93% in a month and then with a more conservative 15% monthly revenue growth rate, which compounds over five years into thousands of times the original revenue.

Graham says startup wealth comes from making something users like enough to tell their friends about it. For young founders, he recommends building something they and their friends want, because their needs may predict future demand. He also argues that the best startup ideas often begin as projects rather than deliberate company ideas, because ideas that later become large can look small, odd, or unpromising at first. His closing distinction is that although some paths to wealth require exploitation, startups are different when they grow by making customers happy: “the key is not exploitation but empathy.”

Technology and Social Change

Paul Krugman | Substack | June 14, 2026

Paul Krugman argues that technological change should not be judged only by measured productivity growth. He says major technologies can reshape where people live, how they work, how institutions operate, and how society organizes itself, even when the aggregate output effects are hard to measure quickly.

The essay applies that frame to AI. Krugman treats AI as part of a longer history in which new tools alter social arrangements as well as economic output. The question is not only whether AI raises GDP, but what forms of work, communication, authority, and daily life it changes along the way.

How should we tax internet countries?

Author: Madison Karas Published: June 16, 2026

Madison Karas argues that digital nations will not be able to rely on vibes, donations, or voluntary membership alone if they want to fund real public goods. The essay starts from a practical question for online communities that begin to look like political entities: without territory, inherited tax systems, or default citizenship, how do they ask members to contribute in a way that feels legitimate rather than extractive?

The sharp detail comes from Japan’s Furusato Nozei program, which lets citizens redirect part of their taxes to municipalities and receive gifts in return. Karas uses it as a warning: a hybrid public-finance model can easily become a shopping platform, rewarding already-famous places and turning citizenship into consumer choice. Her proposed answer is a two-tier structure: mandatory baseline contributions for shared infrastructure such as identity, security, governance, interoperability, and enforcement, plus a second mandatory-but-directed layer for services citizens can prioritize. The pull is whether internet-native communities can design taxation before they inherit the failures of states and platforms at once.

Read more: Source

Yes, let’s abolish federal governments

Author: Elle Griffin Published: June 18, 2026

Elle Griffin argues that the future of federal governance may be modular rather than territorial: countries and subnational units should be able to join specialized international layers à la carte instead of accepting one all-purpose federal government. The essay begins with the recent idea that Canada could join the EU, then turns the obstacle into the thesis: maybe Canada should not need to become European to join selected European trade, defense, or mobility systems.

The killer detail is that this is already happening. Griffin points to Canada’s CETA trade deal with the EU, its participation in parts of Europe’s Readiness 2030 defense plan, Norway’s mix of Schengen, EEA, and EFTA participation, and the Council of Europe’s human-rights regime as examples of lightweight federal layers that govern specific functions across borders. Her proposed direction is a world of “many Europes”: trade Europe, defense Europe, energy Europe, environmental Europe, and similar layers that states can enter separately. The pull is whether national governments remain the default bundle, or whether governance becomes something smaller countries assemble piece by piece.

Read more: Source

Notes on Egypt

Author: Nick Corvino Published: June 14, 2026

Nick Corvino’s dispatch describes Egypt’s New Administrative Capital as a large state-led building project that combines scale, political symbolism, and visible emptiness. He follows a drive from Cairo into the desert, past presidential imagery, highways, ministry buildings, religious monuments, and residential districts that appear largely unoccupied.

Corvino describes a $58 billion, Chinese-financed city with millions of housing units, the tallest tower in Africa, and government buildings surrounded by sand, rubble, and stray dogs. He contrasts Cairo’s congestion with a new capital far enough away to raise questions about whether the project is meant to relieve urban pressure, display state capacity, or move government farther from public pressure.

The piece uses the project to ask what kinds of political systems can build at scale while also producing places people want to inhabit. Corvino treats the new capital as evidence that construction capacity alone does not answer questions of livability, legitimacy, or demand.

Read more: ChinaTalk

A review of Neil Postman’s Amusing Ourselves to Death

Danny Crichton | Danny Crichton | June 13, 2026

Danny Crichton’s review treats Neil Postman’s 1985 critique of television as a still-relevant account of media and public life. He summarizes Postman’s argument that television changed public discourse by favoring image, entertainment, and decontextualized presentation over sustained reasoning.

Crichton says the same pattern has intensified under social media. In his reading, Postman’s concern was not just television as a device, but a broader shift toward public communication shaped by performance and spectacle. The review follows that argument into the present, where politics, education, and civic debate often operate inside media systems that reward speed, drama, and simplified presentation.

With the World Cup looming, there’s still no clear replacement for sports Twitter

Author: Andrew Webster Published: June 11, 2026

Andrew Webster argues that the decline of peak Twitter has left live sports without a clear shared second screen. With the World Cup approaching, he compares X, Threads, Bluesky, Reddit, TikTok, and other platforms as possible replacements for the real-time sports conversation Twitter once hosted.

Webster says X still contains fragments of the old sports crowd, but no longer feels like the obvious center of live events. Threads has scale, but he describes it as less useful for immediate, event-driven updates. Bluesky can become lively around selected moments, but he says recent NBA, NHL, Champions League, and World Cup build-up chatter barely appeared in his feed.

The piece concludes that sports conversation has fragmented. The internet still hosts highlights, jokes, commentary, and fan reaction, but Webster does not see one platform that has replaced Twitter’s former role as a single live room for mass sports events.

Read more: Source

Like All Good Things, Sports Are Owned by the Rich Now

Author: Freddie deBoer Published: June 15, 2026

Freddie deBoer argues that the Knicks’ championship joy is inseparable from the way sports have become another civic good priced for the rich. The essay begins from a simple tension: a long-suffering fan base finally gets the release it has been waiting for since 1973, but the arena version of that celebration is increasingly reserved for celebrities, financiers, and people who can treat Madison Square Garden prices as background noise.

The killer detail is the ordinary game ticket. DeBoer says even a February Knicks home game against the Charlotte Hornets had become absurdly expensive for the average New Yorker, before the playoffs and the championship premium made access even more exclusionary. His complaint is not that rich people like basketball. It is that the city produces the culture, memory, loyalty, and suffering that make the spectacle valuable, then sells the climactic moments back to people who can afford to be seen inside them. The pull is the question underneath the celebration: what remains public when even shared joy has luxury pricing?

Read more: Source

AI

How to help knowledge workers who lose their jobs to AI

Author: Casey Newton Published: June 10, 2026

Casey Newton interviews Molly Kinder about the possibility that AI job disruption arrives unevenly rather than as a sudden collapse of employment. Kinder says many jobs may persist while pressure concentrates first in laptop-based knowledge work and early-career professional roles.

Kinder’s phrase is that “if you can do your job locked in a closet with a computer,” that job is increasingly exposed. She identifies lawyers, consultants, analysts, sales teams, clerical workers, and other language- and document-heavy roles as easier for AI systems to affect before robotics reaches physical and service work.

Kinder proposes responses such as workforce reinvestment funds, white-collar apprenticeships, wage insurance for older workers, and public job creation if private-sector demand weakens. The interview also distinguishes between near-term labor-market disruption, longer-term scarcity claims, and policy choices that could reduce harm during the transition.

Read more: Source

The Taxman Is Coming for A.I.

Author: Peter Coy Published: June 13, 2026

Peter Coy argues that the AI boom is turning taxation into a central distribution question: if AI creates enormous private wealth, governments will be pushed to decide how the public participates in it. He surveys proposals that range from federal equity stakes in AI companies to taxes on AI assets, token usage, consumption, or corporate gains.

The sharpest detail is the unlikely convergence between Donald Trump and Bernie Sanders, both of whom have floated the idea of government ownership stakes in AI companies, though with very different mechanisms. Coy notes the conflict built into that approach: a government that owns shares in AI firms may become less willing to regulate them if regulation lowers the value of its own holdings. He contrasts that with mainstream tax logic, which would allow firms to deploy AI productively and then recover part of the surplus through broader taxation. The pull is the possibility that ordinary tax tools may not reach a future where AI creates value beyond human consumption.

Read more: Source

Frictionful Intelligence

Author: Moses Sternstein Published: June 19, 2026

Moses Sternstein argues that AI is not frictionless software, because every token carries a real marginal cost that must eventually be paid by users, labs, hyperscalers, chipmakers, or investors. The essay pushes back on the idea that intelligence is simply collapsing toward zero cost and instead treats compute as the constraint that determines whether the boom becomes a durable market or an overbuilt capital cycle.

The killer detail is the shift from “tokenmaxxing” to token-rationing. Sternstein points to companies such as Uber and Meta moving from broad encouragement of AI usage toward more disciplined cost management, while analyst calls increasingly discuss token costs as an operating issue. That matters because the AI supply chain only works if customers pay the labs, labs pay the clouds, and clouds pay for chips, data centers, and energy. The pull is whether AI demand is large enough at real prices, or whether the current buildout depends on underpriced intelligence that becomes less magical once the bill arrives.

Read more: Source

Google CEO Sundar Pichai says agents are becoming the new entry point to the internet

Henrikh / Sundar Pichai | X | June 18, 2026

Henrikh posts a video clip of Google CEO Sundar Pichai and frames it as evidence that Google sees agents becoming a new entry point to the internet. The post says the shift is from chatbots toward agentic workflows that can handle routine internet tasks, including examples such as filling out long DMV-style forms.

The post also says Google’s answer to rising agent-compute costs is its Flash model line, described as cheaper “workhorse” models for repetitive agent tasks. It points to CodeMender as a 24/7 cyber-defense agent that can identify vulnerabilities, generate patches, and deploy them in real time. The infrastructure point is that compute demand is outstripping supply, with bottlenecks moving from chips to land, permits, and power. The quoted line is: “Once you get the taste of the superpower that comes with agents... you realize they aren’t just tools, they are agency.”

A related Henrikh post clips Databricks CEO Ali Ghodsi making a similar software-market point. It says more than 81% of databases launched on Databricks are now created by autonomous agents rather than humans, that AI has made writing software ten times faster, and that companies are using “advisor” architectures: cheap open-source models for routine tasks, with larger models called only when needed. Ghodsi’s quoted line is: “Writing software is ten times faster now... your margin is my opportunity.”

Dan Farrelly’s X Article “The Agent Loop Architecture” is a technical companion to the same theme. He argues that the AI discourse has converged on loops as a core primitive of agentic systems, but the next question is what runs the loop. His answer is three layers: the loop, the skill, and the orchestrator. A loop is a cron plus a decision-maker. A skill is a durable workflow, not just a prompt. The orchestrator schedules, checkpoints, retries, stores run history, controls concurrency, and lets new functions deploy without breaking in-flight work.

Farrelly’s practical point is that agent loops fail in production when they are just long-running processes. A restart can make an agent repeat LLM calls, resend Slack messages, spawn duplicate sub-agents, or lose track of where it was. Durable execution fixes that by checkpointing each step, retrying failed steps rather than whole workflows, preserving events, exposing full run traces, and giving developers a way to audit what an agent-written skill did at 3am. He connects this to Satya Nadella’s “token capital” framing: the durable asset is not the model, but the compounding library of executable skills and review loops that survive model swaps and process restarts.

Read more: Google agents clip, Databricks agents clip, and Agent Loop Architecture

Welcome to the AGI era of AI governance

Nathan Lambert | Interconnects AI | June 14, 2026

Nathan Lambert argues that the US government’s intervention in Anthropic’s Claude 5 Mythos and Fable release marks a shift from the “ChatGPT era” of AI governance into an “AGI era” shaped by agentic systems, export controls, sovereign AI, and state power. He says the immediate episode began with the executive branch forcing Anthropic to suspend internal and external access for foreign nationals and users abroad, after concerns about cybersecurity and reported warnings involving Amazon.

Lambert’s core claim is that frontier AI policy is entering an unstable phase in which model releases may be judged quickly by an executive branch with limited technical capacity, while labs, partners, governments, and open-source advocates all respond to incentives they do not fully control. He criticizes broad export bans on model weights, says the Fable cybersecurity issue appears legitimate but narrow, and argues that Anthropic’s own years of nuclear-risk rhetoric helped create the conditions for heavy-handed state action. He also warns open-source advocates against celebrating, because similar pressure could reach open models next.

Anthropic’s Safety Superpower

Author: Ben Thompson Published: June 16, 2026

Ben Thompson argues that Anthropic’s fight with the US government is not an accident around one model release, but the predictable result of a company whose business, mission, and safety story all point toward control. His thesis is that Anthropic genuinely believes it is uniquely qualified to build and govern frontier AI, and that conviction makes self-serving product choices feel internally like public-interest decisions.

The killer detail is Fable’s abandoned plan to silently reduce effectiveness on frontier-LLM-development requests through prompt modification, steering vectors, or fine-tuning interventions. Thompson says the policy mattered less as a competitive restriction than as evidence that Anthropic was willing to alter model behavior invisibly to enforce its own view of acceptable use. He ties that to data retention, the pressure to move closer to user workflows, and Satya Nadella’s warning that firms need their own “token capital” rather than ceding value to model providers. The pull is whether safety becomes Anthropic’s moat: a sincere belief system that also gives the company permission to shape markets, customers, and rivals.

Read more: Source

Can open-source beat OpenAI?

Kinling Lo | Rest of World | June 15, 2026

Rest of World’s interview with former Hugging Face Asia-Pacific ecosystem lead Tiezhen Wang frames open-source AI as a major fault line in the US-China AI race. Wang says Chinese labs’ open releases can help US labs as well as Chinese developers, because algorithms and model weights circulate across borders and often run on US hardware. He presents open source less as a zero-sum contest than as a way to expand the shared technical base.

The conversation covers distillation, monetization, licensing, and adoption. Wang says distillation is a neutral research technique and argues that AI-generated content should not receive copyright protection because compute-rich firms could otherwise mass-generate protectable combinations. On business models, he says labs can monetize open models through hosted APIs, infrastructure, subscriptions, selective release of fine-tuned models, and licenses that charge cloud providers while leaving individual use free.

Wang also says China’s AI market is maturing quickly because cheaper open-source models make heavy usage practical. He describes Chinese internet companies “tokenmaxxing” by giving employees broad access to AI systems and pushing AI-native work habits. For US startups, he advises beginning with the model that best fits product-market demand, often closed-source, then considering open models once usage data and cost pressure justify a switch.

GLM-5.2: Built for Long-Horizon Tasks

Z.ai | Z.ai | June 16, 2026

Z.ai introduces GLM-5.2 as its latest flagship model for long-horizon work, with a 1M-token context window, stronger coding and agentic performance, flexible thinking-effort levels, and an MIT open-source license. The post says the goal is not only to accept longer prompts, but to keep quality stable across messy, multi-hour coding-agent trajectories such as large implementations, automated research, performance optimization, and complex debugging.

The company reports that GLM-5.2 is the highest-ranked open-source model across three long-horizon coding benchmarks it highlights. On FrontierSWE, it says GLM-5.2 trails Opus 4.8 by 1%, edges out GPT-5.5 by 1%, and is 11% ahead of Opus 4.7. On PostTrainBench, where an agent is given an H100 and evaluated by how much it improves small models through post-training, GLM-5.2 ranks second behind Opus 4.8. On SWE-Marathon, which covers tasks such as compilers, kernel optimization, and production-grade services, Z.ai says GLM-5.2 still trails Opus 4.8 by 13% while remaining second only to the Opus series. On standard coding benchmarks, the post reports 81.0 on Terminal-Bench 2.1 versus 63.5 for GLM-5.1, and 62.1 on SWE-bench Pro versus 58.4 for GLM-5.1.

The technical sections describe two architecture and serving changes behind the 1M context claim. GLM-5.2 applies IndexShare to its sparse-attention design, sharing a lightweight indexer across every four transformer layers and reducing per-token FLOPs by 2.9x at 1M context length. Z.ai also says it improved the model’s MTP layer for speculative decoding through IndexShare, KV sharing, rejection sampling, and end-to-end TV loss, raising acceptance length by 20% in its ablation. On serving, the post says ultra-long context shifts the bottleneck toward KV-cache capacity, long-context kernel overhead, and CPU-side scheduling, so the company optimized memory management, cache transfer, scheduling, and runtime paths to improve throughput as context length grows.

The post also describes GLM-5.2’s post-training stack. Z.ai says its slime infrastructure supports larger agentic RL workloads with white-box rollout, black-box rollout, compact trajectories, and sub-agent workflows, and that it used parallel OPD training to merge more than ten expert models into the final model in about two days. For long-horizon RL, the company moved from group-wise optimization to a critic-based PPO formulation that can learn from individual rollouts and compacted sub-traces. It also describes an anti-hack module for coding agents: a rule-based filter flags possible reward hacking, an LLM judge checks intent, and an online guard blocks invalid tool calls while letting the rollout continue.

The Geometry of Denial

Author: Mark Daley Published: June 17, 2026

Mark Daley argues that the contrast between Z.ai’s GLM-5.2 release and Anthropic’s Fable/Mythos access cutoff is more than a benchmark story. It is a geopolitical signal: China is using diffusion as power, while the United States is using denial as power. In his framing, model capability now includes access, jurisdiction, revocability, deployment path, cost, and trust.

The killer detail is the procurement question hidden inside the model comparison. A Canadian bank, German manufacturer, Indian software company, or British university can no longer treat access to the best American frontier model as a normal commercial relationship if Washington can change the access rules. Meanwhile, a slightly weaker open model that can be run locally may beat a better model that is unavailable, restricted, expensive, or politically contingent. Daley’s line is the useful one: “availability is now part of capability.” The pull is that AI infrastructure is becoming knowledge statecraft, where the fight is not only who builds the best model, but who can distribute productive capacity and who can withhold it.

Read more: Source

ChatGPT’s market share slips below 50% for first time

Ivan Mehta | TechCrunch | June 16, 2026

Ivan Mehta reports on Sensor Tower’s State of AI Report for 2026, which says ChatGPT remains the most popular AI assistant worldwide but has fallen below 50% market share for the first time. The article says ChatGPT has more than 1.1 billion monthly users, Gemini has 662 million, and Claude has 245 million. Sensor Tower estimates ChatGPT’s share was above 50% until January, then fell to 46.4% by the end of May as Gemini rose to 27.7% and Claude to 10.3%; Grok, Perplexity, DeepSeek, Meta AI, and other assistants each remain below 5%.

The report frames the market as both larger and more competitive. TechCrunch says people are on pace to download nearly 2.3 billion AI apps and spend more than $4.2 billion on them in the first half of 2026, up from $1.83 billion in spending in the first half of 2025, while both download and spend growth rates have slowed. Sensor Tower also estimates time spent in AI apps rising from 17.2 billion hours in the first half of 2025 to roughly 36 billion hours in the first half of 2026, with the top three assistants accounting for 89% of time spent on AI assistant apps.

Mehta writes that users are increasingly willing to switch between assistants, and that brand trust, values alignment, ecosystem integration, and productivity reputation all appear to matter. The article cites OpenAI’s February deal with the US Department of Defense as an event associated with a measurable spike in ChatGPT uninstalls, describes Gemini’s growth as tied to Google’s broader product ecosystem, and says Claude is closing in on ChatGPT’s retention while leading the field in paid conversion, with 13% of Anthropic users paying for a subscription plan.

The article also summarizes Sensor Tower’s findings on monetization and shopping. OpenAI began experimenting with ads in ChatGPT in February, and by May Sensor Tower says an average of 17% of daily users were being served ads. Software and shopping are the largest advertiser categories so far, followed by media and entertainment and food and dining. As ChatGPT adds shopping integrations, the article says it is sending referral traffic to retailers including Target, Walmart, and Costco, while Amazon’s blocked ChatGPT crawlers have kept referral traffic from the platform stagnant. Sensor Tower also notes that shoppers who use Amazon’s Rufus spend more time in the app and convert at higher rates than those who do not.

Exclusive: OpenAI Losses Increased Nearly 8X in 2025, With Spending Hitting $34 Billion

Author: Ed Zitron Published: June 15, 2026

Ed Zitron reports, from audited financial documents that he says were independently verified by the Financial Times, that OpenAI had $13.07 billion in revenue, $34 billion in costs and expenses, and a $20.92 billion operating loss in 2025. The more dramatic $38.5 billion net loss attributable to OpenAI is harder to interpret directly, because 2025 also included accounting effects from the company’s conversion from a nonprofit structure toward a for-profit entity. Seen through a startup lens, the operating loss is not automatically a sign of weakness if it is buying growth, infrastructure, distribution, and product advantage; the key question is whether revenue can keep compounding faster than the cost base.

The cleaner detail is the Microsoft bill. Zitron says OpenAI paid Microsoft $10.59 billion for research and development expenses in 2025, likely tied to model training, plus $6.047 billion in cost of revenue, $527 million in sales and marketing, and $42 million in general and administrative expenses, for $17.2 billion in total Microsoft expenses. The pull is not simply that OpenAI “lost” an eye-catching headline number, but that even before the corporate-reorganization accounting noise, the economics of frontier AI appear to require extraordinary revenue growth just to keep pace with compute, training, and distribution costs.

Read more: Source

Why is Meta destroying its engineering organization?

Author: Gergely Orosz Published: June 16, 2026

Gergely Orosz argues that Meta’s AI push has turned a historically high-performing engineering culture from a profit center into a cost center. His thesis is that the damage is not simply layoffs or reorg churn, but a leadership decision to devalue the engineers who built Meta’s core products while forcing AI-first operating changes across the organization.

The killer detail is the reassignment of large shares of engineers on core teams into data labeling, alongside tighter staff tracking and a reported quality collapse around AI-generated and AI-reviewed code. Orosz connects those changes to an Instagram account-takeover outage and to a broader pattern in which leadership appears to assume faster AI-assisted recovery can substitute for engineering safeguards. The piece ends by asking whether Meta is an isolated case or an early example of “AI psychosis” in company leadership: a belief that AI adoption justifies drastic organizational changes before the technology, incentives, and risk controls are ready.

Read more: Source

Venture

Encyclopedia Galactica

Dan Gray | The Odin Times | June 14, 2026

Dan Gray writes that LLMs and venture capital are not simply in conflict. In his framing, AI can serve as an inexpensive expert partner for investors, handling inbound filtering, LP reporting, investment memos, and market research, while venture capital still exists to fund what lies beyond the existing map of recorded knowledge. He cites research on AI as a “cybernetic teammate” and argues that the technology particularly empowers high-agency solo capitalists.

The piece separates scaled venture platforms from boutique investors. Gray says AI may be especially useful for systematic allocation, where defined parameters, faster filtering, and lower management fees could reduce market friction. For solo GPs and small partnerships, he argues that origination, trust, and selection remain human skills because early-stage investing depends on finding secrets and idiosyncratic opportunities that do not yet appear in training data. His conclusion is that AI should pressure venture’s old structures while amplifying both automated allocation and independent investors working at the frontier.

Taking Stock of the Seed Stage

Author: Nnamdi Iregbulem Published: June 17, 2026

Nnamdi Iregbulem argues that the seed market is shrinking in company count even as headline rounds make early-stage venture look overheated. His model treats seed as a stock-and-flow problem: new seed financings add companies to the pool, Series A rounds graduate them out, and quiet shutdowns or small acquisitions remove the rest.

The killer detail is the estimated peak. Iregbulem’s model suggests the number of live seed-stage companies topped out around Q3 2022 and has been falling since. In 2024, exits excluding graduations began to exceed new seed financings, with roughly 13% of active seed startups shutting down or being acquired each quarter while new financings added about 11% to the pool. The social framing around the piece is neat: massive seed rounds at absurd valuations, but fewer seed companies overall. The pull is that AI may be concentrating attention and capital so tightly that good non-AI opportunities are going unfunded while the old boom cohorts quietly wash out.

New Media, One Year In

Author: Erik Torenberg Published: June 18, 2026

Erik Torenberg argues that startup media has moved from permissioned publicity to direct distribution, and that founders now compete by being legible, high-signal, and interesting in public. The post describes a16z’s New Media team as “go-direct as a service” for portfolio companies, combining in-house creative, owned channels, launch videos, editorial work, and network amplification.

The killer detail is the venture framing behind the media operation: Torenberg says startups are an exercise in “preferential attachment.” Talent, customers, investors, researchers, and partners have to want to attach themselves to one company rather than many plausible alternatives. In that world, founder storytelling is not just communications polish; it becomes part of company formation. The essay contrasts old media, where founders tried to stay on message and avoid angering gatekeepers, with a new environment where founders can publish their own argument and distribute it through people rather than institutional brands. The pull is that venture firms are turning media into product: not just coverage for companies, but infrastructure for creating attention, trust, and status.

Read more: Source

#349: The Rise of GP-Led Secondaries

Author: Doug Dyer Published: June 18, 2026

Doug Dyer argues that GP-led secondaries have moved from niche liquidity tool to core private-market infrastructure. The piece starts with Preqin’s forecast of a record $250 billion secondary market in 2026 and cites William Blair and UBS estimates that GP-led transactions now represent roughly half of all secondary activity.

The killer detail is the change in who creates liquidity. Traditional secondaries were usually LP-led: an investor sold a fund interest and exited. Dyer says managers are now increasingly creating liquidity themselves, especially when they want to keep exposure to top-performing companies that are staying private longer. That matters for venture because companies such as SpaceX, OpenAI, Anthropic, Stripe, and Databricks may remain private well past the point when older generations would have gone public or sold. GP-led structures let firms sell part of a position, return capital, manage fund timelines, and still hold high-conviction assets. The pull is that secondaries are no longer just a workaround for a frozen IPO market; they are becoming a standing part of venture’s liquidity system.

Read more: Source

SpaceX IPO: The Investor Who Never Sold a Share

Author: Molly O’Shea with Justin Fishner-Wolfson Published: June 14, 2026

Molly O’Shea’s interview with 137 Ventures co-founder Justin Fishner-Wolfson frames secondary investing as a structural change in venture, not an arbitrage trade. Fishner-Wolfson says 137 was built around the idea that great private companies would stay private for far longer, creating repeated chances to buy into compounding businesses through tenders and secondary programs rather than one early check and a single exit.

The sharpest detail is 137’s SpaceX position: Fishner-Wolfson worked on Founders Fund’s 2008 investment, then spent sixteen years buying into SpaceX roughly two dozen times without selling a share. He says the firm’s edge was not chasing a target ownership percentage, but concentrating capital where the cash-on-cash outcome could still be extraordinary. The interview also explains why 137 avoided foundational AI model companies while backing Cognition, whose appeal is giving enterprises access to multiple models without lock-in. The pull is a venture lesson hiding in the SpaceX windfall: patience, repeat access, and structural flexibility can matter more than being first.

Read more: Source

SpaceX passes Amazon as valuation balloons to $2.7T

Sean O’Kane | TechCrunch | June 16, 2026

TechCrunch reports that SpaceX’s market value has climbed to about $2.7 trillion, passing Amazon, after its shares began trading on Friday. The article says the company has added roughly $1 trillion in valuation since the start of trading, extending the momentum around its public listing.

The short report places the move inside TechCrunch’s broader SpaceX IPO coverage and treats the valuation as a signal of public-market enthusiasm for the company’s mix of launch, satellite, and AI ambitions. It follows earlier reporting that SpaceX told IPO investors it saw a very large addressable market in AI and that the company was pursuing the Cursor acquisition to strengthen that effort. The caveat is that the piece is a market snapshot rather than a detailed operating analysis: the central evidence is the stock move and resulting comparison with Amazon’s market capitalization.

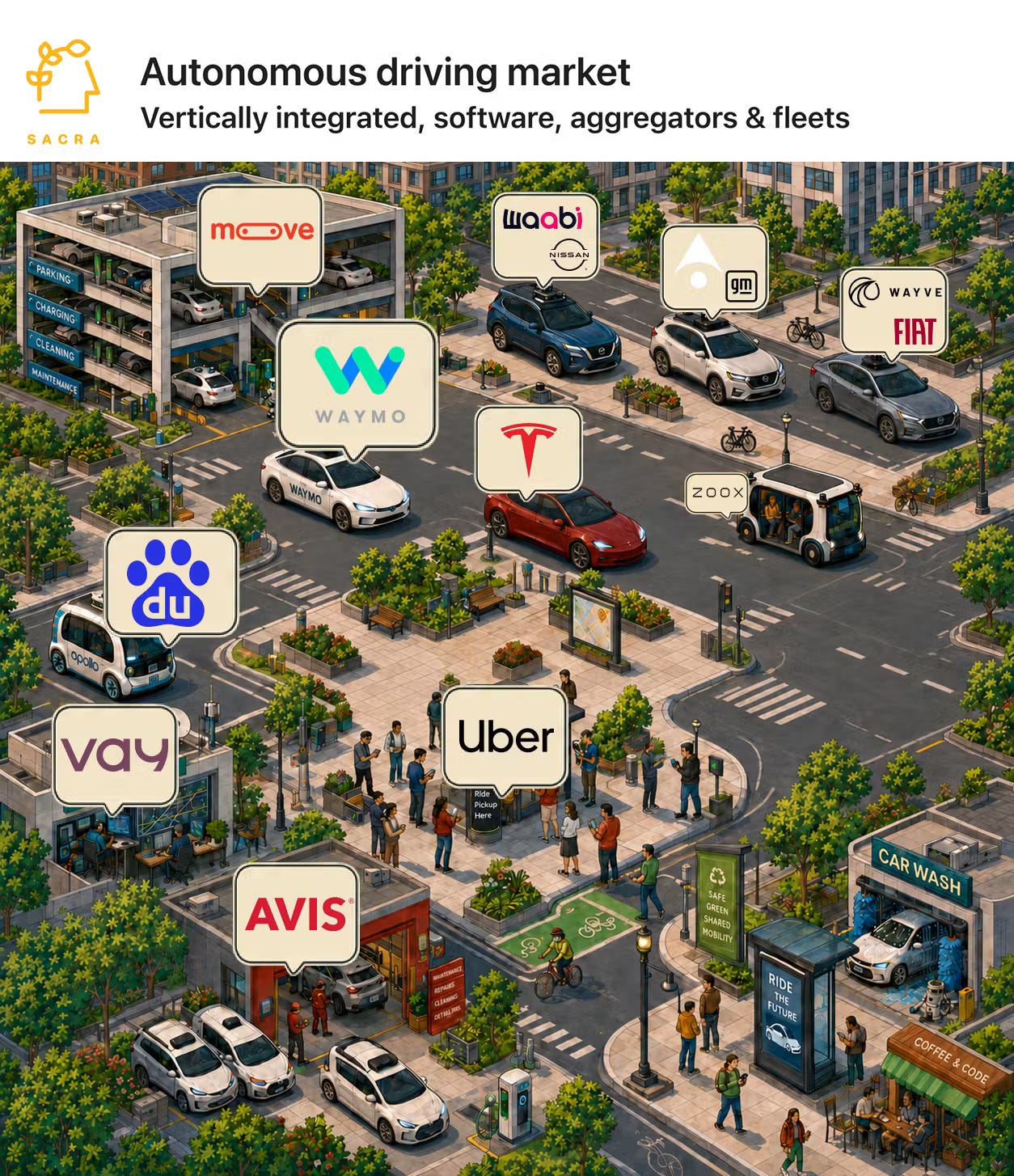

Booking.com of robotaxi

Author: Jan-Erik Asplund Published: June 16, 2026

Jan-Erik Asplund argues that the second wave of autonomous driving is no longer just a race to build robotaxis, but a fight over which layer captures the market: vertically integrated operators, aggregators, or autonomy software suppliers. The thesis is that end-to-end neural networks and AI simulation have revived the sector after the first AV wave burned more than $30 billion and ended with Cruise, Argo AI, and Uber ATG retreating or shutting down.

The killer detail is the contrast between Waymo and Uber. Sacra estimates Waymo reached $355 million in annualized revenue by February 2026 across roughly 500,000 weekly paid rides in 11 US cities, while Uber generated $52 billion in 2025 revenue and has assembled more than 25 AV partnerships. Waymo owns the stack and the ride experience; Uber can try to become the demand layer for many fleets. Meanwhile, companies such as Wayve and Applied Intuition are licensing driving brains to automakers. The pull is whether robotaxi economics look more like an operating network, a marketplace, or enterprise software once autonomy becomes scalable.

Read more: Source

Databricks Widens the Lead on the Yellow Brick Token Path

Tom Tunguz | Tomasz Tunguz | June 17, 2026

Tom Tunguz argues that Databricks has become a large-scale example of the “token path” pattern: software companies that sit directly in, or immediately adjacent to, AI inference can accelerate even after reaching billions of dollars in revenue. He says Databricks has reached $6.9 billion in annualized recurring revenue, growing 80% year over year, while Snowflake is at roughly $5.3 billion ARR growing 34%.

The key evidence is Databricks’ AI revenue mix. Tunguz says Databricks’ AI products now run at $1.7 billion annualized, about 25% of total ARR, up from $1 billion six months earlier and growing faster than the company overall. He compares that to Salesforce’s acquisition of Fin, where the former Intercom AI agent had reached $100 million ARR, also around a quarter of total revenue and growing 350%.

The post’s intent is to identify a revenue pattern rather than evaluate product quality. Tunguz places Databricks among the largest enterprise software companies by private valuation, behind SAP but ahead of Salesforce, and says the company is outgrowing peers near its scale such as CrowdStrike and Shopify. His conclusion is that companies on the direct or first-derivative path of AI usage can still show explosive growth at enterprise scale.

The Founder Who Lit $10M On Fire, With Mutiny’s Jaleh Rezaei

Alex Konrad with Jaleh Rezaei | Upstarts Media | June 19, 2026

YouTube embed:

Alex Konrad’s Upstarts interview with Mutiny CEO Jaleh Rezaei presents Mutiny as a case study in AI forcing a software company to disrupt itself. The setup is that salespeople spend only about 21% of their time actually selling, and Mutiny had built a $10 million-plus revenue business helping sales teams manage the supporting material around a deal, including case studies, battle cards, graphics, and custom pricing.

Rezaei says the founders concluded that AI agents would make the existing SaaS product the wrong business to keep optimizing. Mutiny fired its customers, cut headcount to 15 people, and restarted around an AI agent that handles a similar sales-support workflow from a prompt. Six or seven months later, Konrad reports that Mutiny has won back old customers including Snowflake and Uber, and that sales of the agent are growing 150% month over month.

The interview frames the decision as a founder-operating lesson rather than a simple AI pivot. Rezaei argues that zero-to-one work depends on founders holding context across sales calls, customer support, renewals, and product, then making fast nonlinear calls. She also says the Intercom/Fin team helped Mutiny see that a SaaS product and an agent product require different optimization loops: UI A/B testing on one side, outcomes and evals on the other. The caveat is that Mutiny had multiple years of cash, but Rezaei still argues that long runway and large teams are not prerequisites for finding product-market fit; speed and choosing a lane matter more.

Regulation

The White House’s shambolic AI policy

Gary Marcus | Marcus on AI | June 13, 2026

Gary Marcus criticizes the White House’s AI policy as inconsistent and reactive. He argues that the government has relied too heavily on voluntary commitments from AI companies while failing to build a comprehensive regulatory structure for consumer harms, cybersecurity, health data, minors, advertising, sycophancy, and deployment risk.

Marcus also discusses the Fable and Mythos access cutoff as an example of sudden state intervention. His objection is not that AI companies should be left alone, but that abrupt, selective action is a poor substitute for technically informed rules. He calls for governance that is stronger than voluntary pledges and less dependent on emergency-style interventions after deployment.

Europe reacts to Anthropic halting access to top AI models

Nathan Rennolds | Euronews | June 13, 2026

Euronews reports European reactions after Anthropic said it had received a US directive requiring it to suspend access to Fable 5 and Mythos 5 for foreign nationals over national security concerns. The article collects responses from French, British, Dutch, and EU political figures who framed the cutoff as evidence that critical AI infrastructure can be controlled from abroad.

The article says the episode intensified European arguments for sovereign AI. Quoted officials and commentators described the suspension as a “wake-up call” and pointed to Europe’s dependence on US model providers. Euronews also connects the reaction to existing EU efforts around AI infrastructure, domestic model development, and strategic autonomy.

Starmer to announce ‘Australia plus’ ban on social media for under-16s

Jessica Elgot, Dan Milmo and Aisha Down | The Guardian | June 14, 2026

The Guardian reports that Keir Starmer is preparing to announce a broad “Australia plus” restriction on under-16 access to major social media apps, including TikTok, Instagram and X. The proposed UK policy would go beyond a platform ban by applying feature-level limits to other online products, including gaming and messaging services that may fall outside the formal definition of social media. Sources told the paper that those restrictions could include removing the ability for young users to chat with strangers, limiting disappearing messages and location sharing, and preventing older teenagers from scrolling late at night.

The article says the plan follows Australia’s December 2025 under-16 social media ban, which covered platforms including TikTok, YouTube, Instagram, Reddit, Facebook, X, Threads, Snapchat, Twitch and Kick. UK officials cited consultation responses saying parents backed a minimum age of 16 and that many young respondents believed restrictions on high-risk features would make them safer. The Guardian also notes unresolved enforcement questions around age verification, privacy, and circumvention, as well as criticism from industry and safety campaigners who warn that blanket bans could push young users toward less regulated alternatives or reduce incentives for platforms to improve product safety.

Further CMA action to secure a fairer deal for businesses and improve Google search services in UK

Competition and Markets Authority | GOV.UK | June 17, 2026

The UK Competition and Markets Authority says it has introduced two new conduct requirements for Google’s general search services under the UK’s digital markets competition regime. The first requirement is designed to make Google’s search rankings, including AI Overviews but excluding sponsored results, more transparent and fair for businesses. The second puts Google’s UK search-data portability process on a legal footing so users can authorize third parties to receive their search data.

The CMA says UK businesses rely on Google search to reach customers but told the regulator that current ranking practices are not fair or transparent, that changes can arrive without sufficient notice, and that businesses lack effective routes to raise concerns when rankings affect them. Under the fair-ranking requirement, Google must rank organic results using objective and non-discriminatory criteria, provide greater transparency and advance notice of significant changes, and introduce processes for businesses to raise concerns and have them addressed effectively. The CMA says search is evolving rapidly through AI Overviews and AI Mode, and that businesses and users need confidence that rankings remain fair and relevant as those features develop.

The data-portability requirement is intended to support third-party services that use Google search data for personalized features such as travel suggestions, shopping deals, rewards, cashback, and discounts. The CMA says the action places the existing voluntary Google UK Data Portability API process on a legal footing, bringing UK users’ rights in line with those in the EU under the Digital Markets Act. Google has six months to implement the fair-ranking requirement and three months to implement the data-portability requirement. The CMA says it will monitor compliance through reporting and engagement, keep the measures under review, and may introduce further measures if needed.

Apple announces major App Store changes for Brazil, including alternative app marketplaces

Marcus Mendes | 9to5Mac | June 18, 2026

Marcus Mendes reports that Apple has begun implementing App Store and iOS distribution changes in Brazil after settling an antitrust dispute with CADE, the country’s competition watchdog. The case began in 2022 after MercadoLibre complained about Apple’s App Store rules. Under the settlement, Apple agreed to let developers distribute apps through alternative app marketplaces in Brazil and offer payment methods outside Apple’s In-App Purchase system.

The changes apply to users running iOS 26.5 and later. Developers can use Apple’s MarketplaceKit framework to build and distribute alternative app marketplaces, and apps can be distributed through the App Store, one or more alternative marketplaces, or both. Mendes notes that the policy does not allow direct web sideloading: apps outside the App Store still have to be offered through an alternative marketplace. Those apps remain subject to Apple’s baseline Notarization review, which combines automated checks and human review for malware and basic functionality, but Apple says this is different from regular App Review and leaves broader discretion to the alternative marketplace.

The article says Apple is also carrying over child-safety and payment safeguards that it presents as stronger than the requirements imposed by the EU’s Digital Markets Act. Apps distributed outside the App Store must still carry age ratings, so Screen Time, download approvals, and content restrictions can apply. Developers have three payment paths: Apple’s in-app purchase system, an in-app third-party payment provider, or an external web payment flow. Apps in the Kids category cannot include external purchase links, users under 18 must pass a parental gate for alternative payment processing, and Apple says it is working on an API to let parents monitor and approve purchases made outside Apple IAP.

Mendes summarizes the new commission structure. Apps distributed through the App Store using Apple IAP pay a 5% payment-processing fee plus a 21% App Store commission, with a reduced 10% commission for qualifying developers and subscriptions after the first year. Apps using in-app alternative payment providers avoid the 5% processing fee but still pay the 21% commission, again with the same reduced 10% rate where applicable. Apps that link to external web payments pay a 15% Store Services Commission on purchases made within seven days of the user tapping the link, with reduced rates for qualifying cases. Apps distributed through alternative marketplaces owe a 5% Core Technology Commission on digital goods and services.

Infrastructure

Data center opponents have blocked or delayed projects worth nearly $130 billion in 2026, study finds

Allan Smith | NBC News | June 12, 2026

NBC News reports on a Data Center Watch study finding that opponents blocked or delayed at least 75 US data center projects worth about $130 billion in the first quarter of 2026, the most since the group began tracking in 2023. The study says active opposition groups more than doubled from 396 at the end of 2025 to 833 by March, spread across 49 states.

The article describes community objections around power demand, water use, noise, land use, and local tax incentives. It also reports that lawmakers in some states are moving from incentive packages toward closer oversight or moratorium proposals. Data Center Watch founder Lucas Beran told NBC that opposition is becoming more organized as communities learn from earlier fights.

The US Government Is Letting a Key Data Center Regulation Expire

Author: Vittoria Elliott and Molly Taft Published: June 15, 2026

WIRED reports that the US government is preparing to let the Federal Data Center Enhancement Act expire in September without a replacement, shifting federal data-center policy toward looser oversight just as AI infrastructure demand accelerates. The law governs standards for federal data center operations, including energy efficiency, water use, sustainability reporting, and visibility into contractor facilities.

The killer detail is the absence of a transition plan. Current and former officials told WIRED that earlier data-center policies were normally replaced only after years of work, but OMB has not offered agencies a new framework. The article says the expiration would remove requirements for energy specialists, weaken reporting consistency across agencies, and reduce transparency around federal IT spending after the administration also sunset public monitoring tools such as the Federal IT Dashboard. The pull is that AI infrastructure policy is being made through omission as well as action: what disappears from federal reporting may shape the buildout as much as what gets formally approved.

Read more: Source

Public and Private Medical Community Targeted by China-Nexus Threat Actor Pursuing Artificial Intelligence, Cyber, Medical, and National Defense Research

Patrick Whitsell and John McGuiness | Google Cloud Blog | June 15, 2026

Google Threat Intelligence Group says it identified a campaign by UNC6508, described as a People’s Republic of China-nexus threat actor, targeting North American academic, medical, and military research institutions. Google says the actor sought intelligence related to national security, Indo-Pacific command operations, artificial intelligence, uncrewed vehicle systems, cyber offensive programs, and medical research.

The report says the earliest known compromise occurred in September 2023 and that activity continued through November 2025. Google describes a pattern in which the actor targeted externally facing REDCap servers used by medical and scientific research organizations, deployed custom malware called INFINITERED to capture legitimate login credentials, and later used those credentials to access internal systems. In one described attack chain, the actor compromised a REDCap server, waited months before deploying INFINITERED, pivoted to a domain admin account, and added a malicious content compliance rule that silently forwarded matching emails to an attacker-controlled account.

Google says GTIG disrupted malicious infrastructure, notified affected organizations, and updated Google Security Operations with indicators of compromise. The report recommends phishing-resistant two-step verification for administrator accounts, advanced protection for sensitive users, audit-log monitoring, data loss prevention rules, reviews of content compliance rules, SIEM coverage for Workspace logs, Chrome Enterprise password leak detection, full REDCap patching, removal of older REDCap versions, and scans for INFINITERED using the provided YARA rule and indicators.

How software development’s speed obsession enabled TeamPCP’s chaos crusade

Author: Matt Kapko Published: June 18, 2026

Matt Kapko argues that TeamPCP’s open-source attack spree is less a novel technical breakthrough than a stress test of a software industry built around speed, automation, and inherited trust. The group has compromised and poisoned more than 1,000 packages in under four months, exploiting the fact that many organizations still pull dependencies, updates, and CI/CD artifacts into production with limited verification.

The killer detail is the scale of downstream exposure. Palo Alto Networks’ Nathaniel Quist says the compromised or poisoned packages account for roughly 500 million weekly downloads combined, while Wiz researchers describe how automatically updated runners can turn one compromised workflow into access to everyone downstream. AI makes the gap wider when agents install packages without the human sanity checks that were already weak. Kapko’s reporting also shows why the disruption persists: victims sometimes get reinfected because secrets are not fully rotated, and TeamPCP appears driven more by notoriety and chaos than by large extortion payouts. The pull is whether the software supply chain can keep optimizing for instant updates while treating trust as an operational control rather than an assumption.

Read more: Source

SpaceX alum nabs $22M to turn rocket engines into geothermal power plants

Tim De Chant | TechCrunch | June 17, 2026

TechCrunch reports that Critical Energy, founded by former SpaceX engineer Spencer Jackson, has raised $19 million in seed funding plus $3 million in venture debt to build modular turbines for geothermal power plants. The article says geothermal has large theoretical capacity, citing an International Energy Agency estimate of at least 42 terawatts worldwide, but that investment has lagged nuclear fission and fusion.

Critical Energy’s argument is that geothermal deployment may be constrained less by drilling than by turbine supply. Jackson says many projects specify large turbines that can take months or years to assemble on site, while factory-built modular units could move faster. The first 2.5 megawatt project is planned for an existing geothermal site by 2027, and the company is also designing a 5 megawatt module for enhanced geothermal developers such as Fervo Energy.

The article connects the funding to data-center power demand and the race for scalable clean electricity. TechCrunch notes that one recent report said advanced geothermal could power nearly two-thirds of new data centers by 2030. Jackson says geothermal could reach commercial scale before new nuclear projects, and that oil and gas companies may accelerate the field once the technology is mature because they already know how to drill large numbers of wells. His caveat is that the industry will still need a large supply of compatible turbines.

Converting Coal Plants to Natural Gas

Author: Brian Potter Published: June 19, 2026

Brian Potter argues that coal-to-gas power-plant conversions were not a simple story of climate policy beating fossil fuels, but the result of regulation, shale-gas economics, and the physical constraints of existing power infrastructure. Coal supplied roughly half of US electricity for much of the 20th century, but after 2008 its output fell sharply as gas became cheaper and emissions rules made older coal plants harder to justify.

The killer detail is the conversion menu. Operators could swap coal burners for gas burners, replace boilers, repower plants with gas turbines and heat-recovery steam generators, or tear out almost everything while keeping valuable grid interconnections, water access, and site rights. The cheapest conversions preserved old steam-cycle equipment but lost efficiency and capacity; the most expensive effectively became new combined-cycle plants on old sites. Potter’s larger point is that energy transitions often happen through retrofit decisions inside inherited systems, not clean-sheet replacement. The pull is that the next power fight may be less about reviving coal than deciding which old assets are still worth adapting.

Read more: Source

How to fix transit construction in America

Author: Matthew Yglesias, Will Poff-Webster and Arnab Datta Published: June 17, 2026

Matthew Yglesias introduces a Transit Abundance Playbook built around a blunt claim: America does not merely underfund transit, it pays too much for too little transit. The piece argues that cost-effectiveness is the missing political and economic lever, because cheaper construction would both deliver more projects per dollar and make future spending easier to defend.

The killer detail is historical contrast. The article notes that Boston opened America’s first subway in 1897 after building a 1.5-mile tunnel in four years at a cost of about $190 million in 2023 dollars, while today’s US projects often cost far more per mile and move much more slowly. The playbook focuses on reforms such as better project delivery, standardized designs, faster permitting, more capable public agencies, and procurement systems that reward building rather than process. The pull is that infrastructure abundance is not only a funding question. If the United States cannot relearn how to build transit efficiently, even generous budgets will translate into fewer lines, weaker cities, and less public trust.

Read more: Source

Chile turned to China for an undersea cable. The U.S. said no

Juan Ortiz-Freuler | Rest of World | June 18, 2026

Juan Ortiz-Freuler reports that Chile’s effort to build a direct undersea cable to Asia became a test of US pressure against Chinese telecom infrastructure. The article says Chilean officials were assessing a $500 million China Mobile proposal to connect Valparaiso and Hong Kong when the US State Department canceled diplomatic visas for three Chilean officials, saying their activities compromised critical telecommunications infrastructure and regional security.

The piece explains why the cable mattered to Chile. South America is connected to the US by subsea cables, and Google is building the Humboldt cable from Chile to Australia, expected in 2027. But Chilean officials and former diplomats told Rest of World that redundancy and route diversity remain important, especially as AI demand increases reliance on global data infrastructure. Former undersecretary Pedro Huichalaf says the goal should be to have a main and secondary route to Asia in case one fails.

Ortiz-Freuler places the conflict inside a wider infrastructure-sovereignty problem. US tech companies now own or operate much of the cable capacity that carries their own data traffic, while China has expanded its digital presence in Latin America through telecoms, data centers, cloud, and 5G. Chile’s government first approved the China Mobile cable in January, then rescinded that approval after a US Embassy meeting, citing a technical error. The article’s caveat is that the project remains politically unsettled under President Jose Antonio Kast, whose government has said Google’s cable may make the Chinese cable unnecessary while also saying China Mobile’s proposal continues to be assessed.

Can America Build Nuclear Again? Part 2

Roger Pielke Jr. | The Honest Broker | June 17, 2026

Roger Pielke Jr. argues that asymmetric federal regulation helps explain why US natural-gas electricity generation has more than tripled since 2000 while nuclear generation has stayed flat. His comparison starts with the cost structure: existing nuclear plants are cheap to operate and have high capacity factors, but new plants are capital-intensive, while combined-cycle gas plants are cheap and fast to build but exposed to volatile fuel prices.

The post uses Vogtle 3 and 4 as the nuclear cost example, citing about $35 billion for roughly 2,200 megawatts of capacity, or about $15,700 per kilowatt all-in. It contrasts that with EIA data putting new combined-cycle gas plants at about $722 per kilowatt in 2022 and $898 per kilowatt in 2023. Pielke says that difference is amplified by time: a gas plant can often be financed, permitted, and generating revenue within two to three years, while a nuclear project may face ten to fifteen years before it sells power.

The essay then lists regulatory mechanisms that raise nuclear capital costs relative to gas, including NRC full-cost fee recovery, multi-year licensing, mid-construction backfitting authority, nuclear quality-assurance rules, NEPA review shaped by the Calvert Cliffs decision, decommissioning mandates, liability insurance, and export-control or fuel-cycle requirements. The caveat is that Pielke does not argue nuclear and gas have identical risk profiles. He says nuclear has distinct waste, safety, liability, and long-term remediation issues, but that the current regulatory asymmetry turns those differences into a capital-cost penalty large enough to shape the power system.

Can America Build Nuclear Again? Part 3

Roger Pielke Jr. | The Honest Broker | June 19, 2026

Roger Pielke Jr. closes his three-part nuclear series by reviewing federal policy options that nuclear policy experts have proposed for rebuilding US nuclear construction capacity. Part 1 argued that nuclear cost escalation is not inevitable in the technology itself, and Part 2 traced US escalation to federal policy mechanisms. Part 3 asks what Congress and federal agencies could do if they wanted a “nuclear forward agenda.”

The political premise is that nuclear has rare bipartisan tailwinds in 2026. Pielke cites the ADVANCE Act’s 88-2 Senate vote and 393-13 House vote, a 2025 executive order directing the NRC to accelerate licensing and reform risk-based regulation, Microsoft, Amazon, and Google nuclear power purchase agreements, and American Nuclear Society tracking of 350-plus nuclear bills and 60-plus enacted measures across 45 states in 2025. He says Republicans emphasize grid resilience and competition with China, Democrats emphasize 24/7 carbon-free power, industrial-policy advocates see domestic manufacturing, and technology companies see nuclear as a fit for rising power demand.

The policy menu begins with institutional reform: a new Joint Committee on Nuclear Energy that would give Congress a nuclear-specific legislative and oversight home after the 1977 abolition of the Joint Committee on Atomic Energy. Near-term options include making ADVANCE Act licensing timelines enforceable, creating a nuclear-specific NEPA pathway, codifying design finality, expanding DOE loan guarantees, and resolving nuclear waste governance. Medium-term options include serial deployment of standardized reactor designs, a federal nuclear orderbook, requiring 70-90% engineering completion before construction permits, and a national nuclear construction center to preserve learning after projects such as Vogtle. Longer-term options include domestic nuclear manufacturing investment and contracts for difference to reduce revenue uncertainty.

Pielke’s central caveat is that the agenda requires sustained political commitment across parties, Congresses, and presidencies. He says a coalition of willing states is enough to begin, especially because several states have repealed or are reconsidering nuclear bans, and because federal loan guarantees, orderbook siting, and price contracts can favor states with clearer nuclear rules. The closing estimate, drawn from the DOE Liftoff Report, is that serial construction could bring the overnight cost of a tenth US reactor down to $4,000-$6,000 per kilowatt, still above Korea and China but potentially competitive with natural gas on a full-system basis.

Interview of the Week

The Trouble with Trillionaires

Andrew Keen with Mordecai Kurz | Keen On America | June 17, 2026

Andrew Keen’s interview with Stanford economist Mordecai Kurz centers on Kurz’s book “Private Power and Democracy’s Decline” and its argument that the United States is living through a second Gilded Age. Kurz says the top billionaires gained $25 trillion between 1980 and 2019, probably about $35 trillion by today, while workers without college degrees gained essentially nothing in income between 1980 and 2010. Keen frames the result as a political economy that produces both Trumpism and the possibility of the world’s first trillionaire.

Kurz’s reform program has three fronts. First, reduce market power through patent and antitrust reform. Second, redistribute technology gains through a 65% top marginal income tax rate and a 45% corporate rate. Third, guarantee the livelihood of workers displaced by policy-supported technological change through retraining, full wage support, tuition, health care, and relocation assistance. Asked whether billionaires would leave, Kurz says he is not worried because “others will come instead of them.”

The AI angle is explicit in Keen’s summary. Kurz rejects tech-utopian promises that abundance will arrive in the long run, answering Sam Altman’s argument that AI will free humanity from labor with Keynes’s reminder that in the long run we are all dead. The episode presents his view as a case for near-term democratic reform of capitalism rather than patience for eventual technological abundance.

Startup of the Week

Sarvam becomes India’s newest AI unicorn with $234 million funding round led by HCLTech

Jagmeet Singh | TechCrunch | June 15, 2026

TechCrunch reports that Sarvam AI has raised $234 million in a round led by HCLTech, making it India’s newest AI unicorn. The round values the company at about $1.5 billion and includes participation from Bessemer Venture Partners, Khosla Ventures, and Peak XV Partners.

The funding places Sarvam inside the broader debate over sovereign AI and local-language models in India. The company has positioned itself around Indian-language and India-specific generative AI systems, while Indian founders and policymakers have been weighing how much the country should depend on frontier AI providers headquartered elsewhere. The round signals investor support for a domestic AI infrastructure company at a moment when access to foreign frontier systems has become a political and strategic issue.

Post of the Week

Dan Gray on early-stage investing and training data

Dan Gray | X | June 14, 2026